Rent vs. Buy - The Absolutely Definitive Guide

Q: Is buying a house a good investment? A: Let’s find out.

Perform your own analysis using the free Gizmo Life Planner.

My House

I own a modest home, in a nice neighborhood, which my family has lived in for nearly 30 years. Our kids were born and raised here. Our friends are nearby, it’s safe, and the schools are great. We’ve got amazing neighbors, some of whom have lived here even longer than we have. We can count on them and they can count on us.

Was buying our home a good investment? Absolutely. We bought a home, but more importantly, we bought a community and a place to make memories.

While buying a home will likely be the biggest investment you will make in your lifetime, it is so much more than that. And, should you buy one, how it turns out financially will depend on your specific circumstances — your location, your timing, and even the world around you.

For me, buying a home was never about investing. It was about all those other things.

Still, it’s good to be smart with your money, so let’s focus just on the financial implications of “rent vs. buy”, a topic discussed widely, and sometimes heatedly, across the internet.

Can You Afford to Do It?

I’m going to use a gaggle of numbers for our analysis, all of which I pulled from the internet. The available free sources are sometimes inconsistent, so consider these as estimates. The data also vary quite a lot by state, so we’ll stick with average values from across the U.S. You can use Gizmo Life Planner with whatever numbers you choose.

Here we go.

The average age of a home buyer in the U.S. is 35, and the average salary of a 35 year old is about $60,000. Let’s suppose our analysis is for a young family with two earners, so let’s set the starting dual-income number at $120,000. After taxes (Federal: $11,000 State: $5,000), that leaves about $104,000 or about $8,600 per month to work with.

The average home price in the U.S. in 2024 is $420,000. In order to avoid Private Mortgage Insurance (PMI), we’ll need 20% down, which is $84,000. Saving that amount is no small feat. Since we’ve waited until age 35 to buy, hopefully by then you’ll have it. Next, we’ll need to borrow about $336,000 to pull this off. With taxes and fees, property taxes and so on, we’ll be paying about $2,500 monthly for our mortgage payments. Following the 1% rule for annual maintenance, we’ll need an additional $400/month, which brings our total to about $2,900 / month, leaving about $5,700 for “all the things”.

So it’s doable, but barely, so long as we are OK with used cars and public schools and hamburgers and camping vacations (all of which are familiar to young me). Single income households might have to wait a while longer, or start smaller.

You’ve got to live somewhere, so the alternative is to rent a place. The average rent in the U.S., which varies considerably by state, is about $1,800 for a two bedroom apartment.

So the critical number here is $2,900 minus $1,800, or $1,100, which is the monthly cash flow difference between buying and renting. Assuming we have the wherewithal to invest that extra money wisely, we’d like to figure out if our net worth will be higher at the end of the game (so to speak) by buying versus renting.

There’s one more factor to consider — if we choose to rent, then we should invest that down payment in the stock market rather than buy that boat we’ve been looking at.

Back of the Envelope

There are a few more numbers we’ll need for our analysis:

- Average Inflation in the U.S. — 3.3%

- Average Housing Price Appreciation — 4.8%

- Average 30 Year Mortgage Rate — 7.7%

- Average S&P 500 Return — 10.5%

- Average Treasury Bond Yield — 6.3%

- Average Rent Inflation — 4.4%

Keep in mind these numbers are averages over many years, typically at least 30, and can vary widely by state. While they are not necessarily reflective of your situation, the basic thought process we will use probably is. You can always use Gizmo Life Planner to analyze your particular circumstance.

The most impactful number in the list above is mortgage interest rate. Figure 1 shows historical values. While the current rates of roughly 7% are hard to stomach, they are not unusual, historically speaking. I bought my house in the early ’90s and paid about 7.5%. Check out that 17% interest rate back in 1982. It was like buying a house on a credit card.

The worst financial decision we can make is to rent and then squander the extra $1,100 available to our monthly budget. In my mind, this is the single most important argument in favor of buying a property. It can be a decent investment and it hedges against our natural inclination to spend what we’ve got.

Zoom image will be displayed

Figure 1 — Historical Mortgage Rates https://fred.stlouisfed.org/series/MORTGAGE30US

Perhaps you noticed a conundrum evident in the numbers above. We’ll be borrowing money at 7.7% to purchase an investment that likely yields a return of 4.8%. At first glance, that doesn’t seem like a good idea. But it’s not quite that simple. By purchasing a property we’ll avoid paying rent, which we estimated at $1,800 per month, and that rent will continue to grow with inflation of 4.4%, whereas our mortgage payment will stay the same for 30 years, and then go to zero. And 20 years from now, because of inflation, that mortgage payment will seem like peanuts.

On the other side of that equation, home-related expenses like property tax and maintenance will also grow with inflation. Bottom line — it’s complicated. That’s why we need a tool like Gizmo Life Planner.

Gizmo to the Rescue

Let’s fire up

to help with our analysis. In the first example, I configured Gizmo with a “no house” scenario using the above historical parameters, and invested the extra $1,100 into an S&P 500 index fund earning an average 10% interest compounding annually. For the first case, I also skipped investing our $84,000 down payment.

You’ve got to admit, 10% interest is a very sweet deal, though it comes with market risks. Take a look at the long term historical performance of the S&P 500 index.

Zoom image will be displayed

Figure 2 Historical S&P 500 Returns — https://www.macrotrends.net/2526/sp-500-historical-annual-returns#google_vignette

Overall, it averages out to about 10% annually, but those red years are tough to stomach — especially when there are a lot of consecutive red years. Riding out down markets takes an iron stomach, even with an index fund.

Now let’s see what

The graph below shows our net worth over time for the “rent” option, where we invest the extra $1,100/month into an index fund earning 10%. It’s off to a slow start, but thanks to the power of compounding returns, it really starts to take off after about 20 years. If we keep our lifestyle constant over time (tough, especially if you have kids), we can live off the interest plus social security comfortably at retirement.

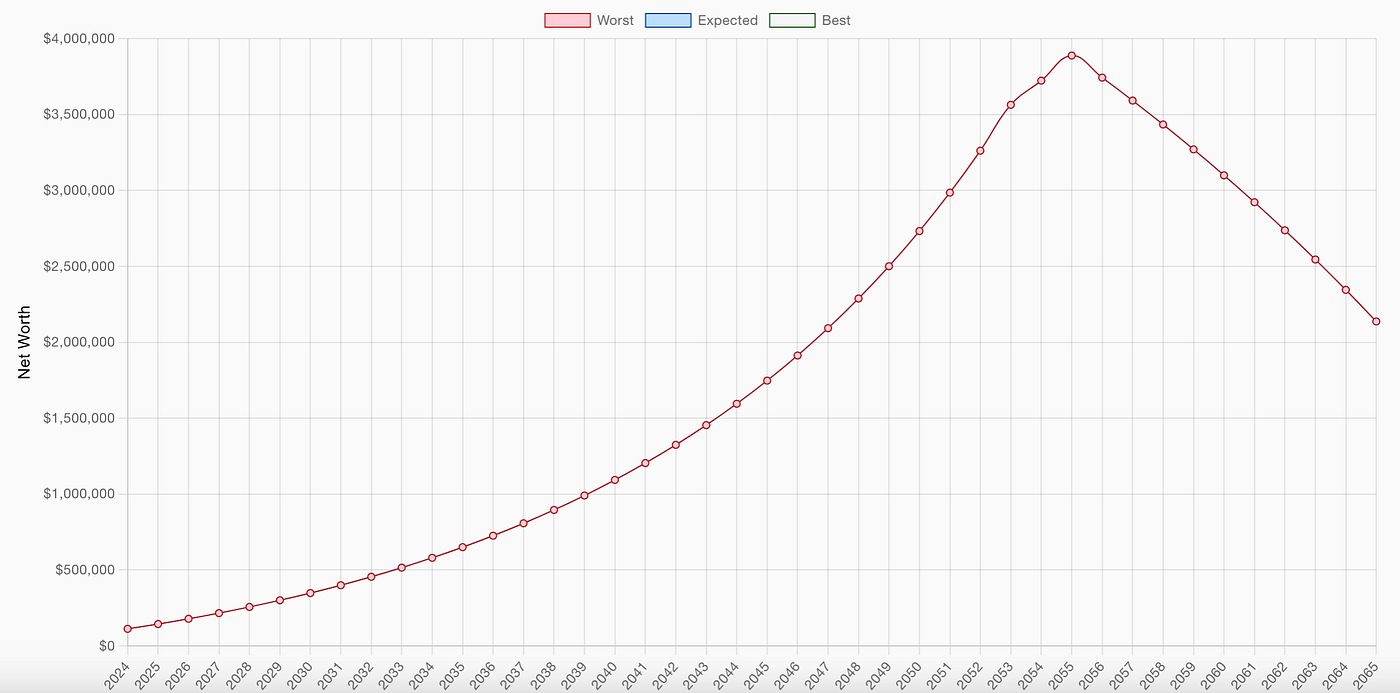

The number we’re most interested in is that at the 30 year mark (year 2054), which is when our mortgage is fully paid.

Zoom image will be displayed

Figure 3–120 K Income, Invest $1,100 at 10% in an Indexed Fund

Now let’s look at the “buy” option, with no additional investments.

Zoom image will be displayed

Figure 4–120K Income, Buy the House

The net worth numbers at the 30 year mark are surprisingly similar, with the buy option ($3.9M) inching out the rent option ($3.6M). The tails of the graphs are quite different, because in the buy option a lot of our wealth is tied up in the property, still increasing at 4.8%. On the other hand, in the rent option our money is still in the stock market, earning away at 10%.

In both cases we’ve probably got enough to ride out our retirement comfortably, but not like royalty. And for the buy option we might need to sell the house and downsize.

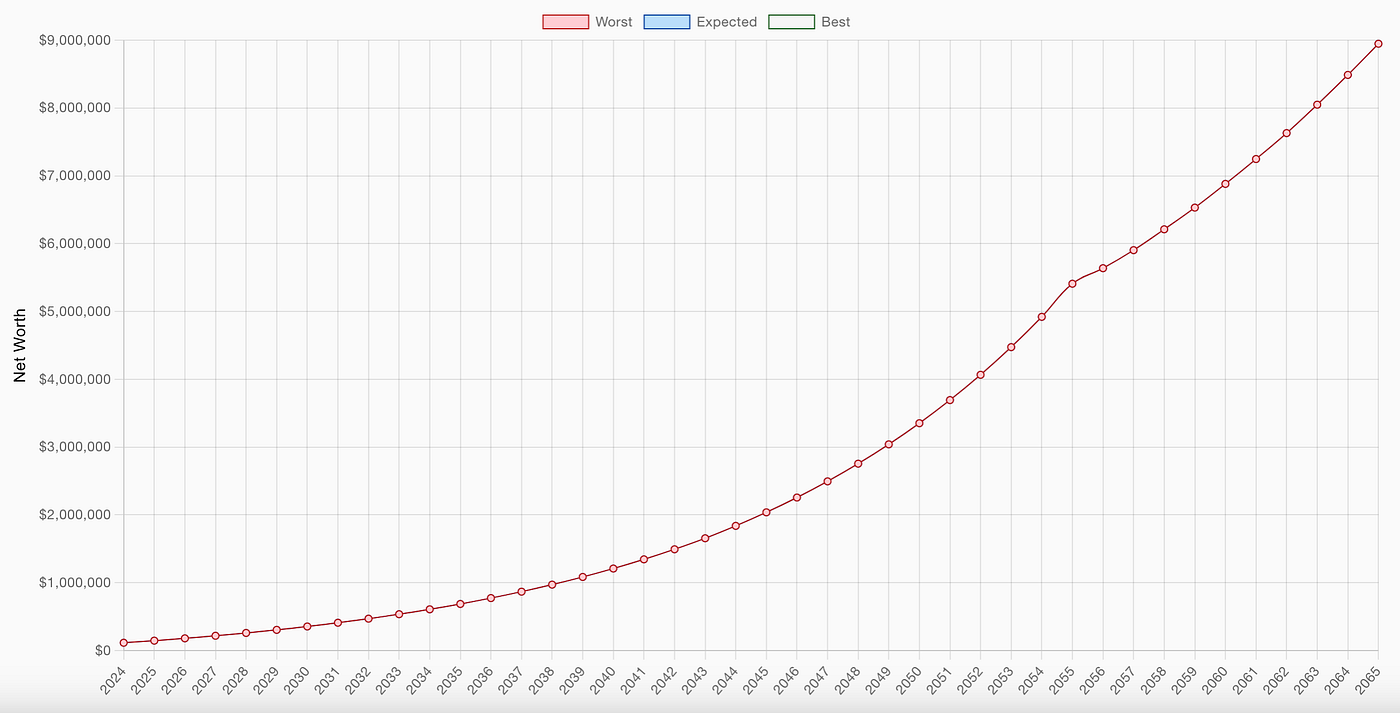

Remember, in the example above, we elected to “buy the boat”, so to speak. What happens if we put that $84,000 into the stock market? In that case we get Figure 5 below.

Zoom image will be displayed

Figure 5 — Rent, and Invest $84,000

Whoa. That’s a lot of money! In this last example, we are basically investing as much as we can reasonably manage into the stock market, and the dividends are clearly rewarding our frugality. Keep in mind though, that these numbers are in the “future value of money”, which sadly is a lot less than the present value of money. We still won’t be rich.

Comparing Investments

Are you suspicious of those results? Gizmo made it quick and easy to generate those graphs, but it also performed a lot of magic behind the scenes. Like including inflation in our budget, starting Social Security at our retirement age, estimating Federal and State taxes, and so on.

Trust, but verify.

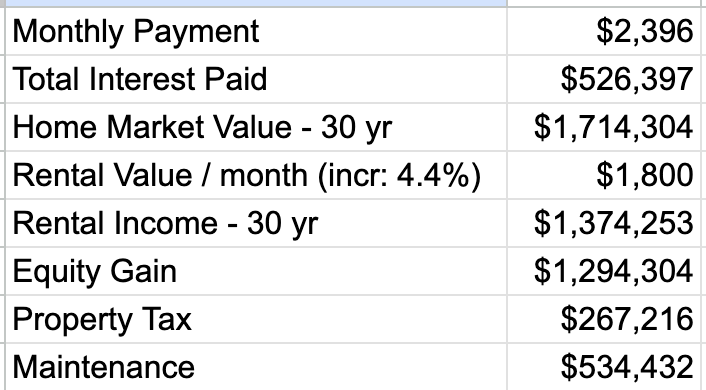

Let’s convert our home investment into an equivalent interest earning investment so we can compare the effective rates of return. We can do this by thinking of our home as a rental property, both appreciating in value and earning $1,800 per month (with rent inflating at 4.4% annually). When we punch these numbers into our trusty spreadsheet, we get numbers like those below (I separated out property tax and maintenance):

Zoom image will be displayed

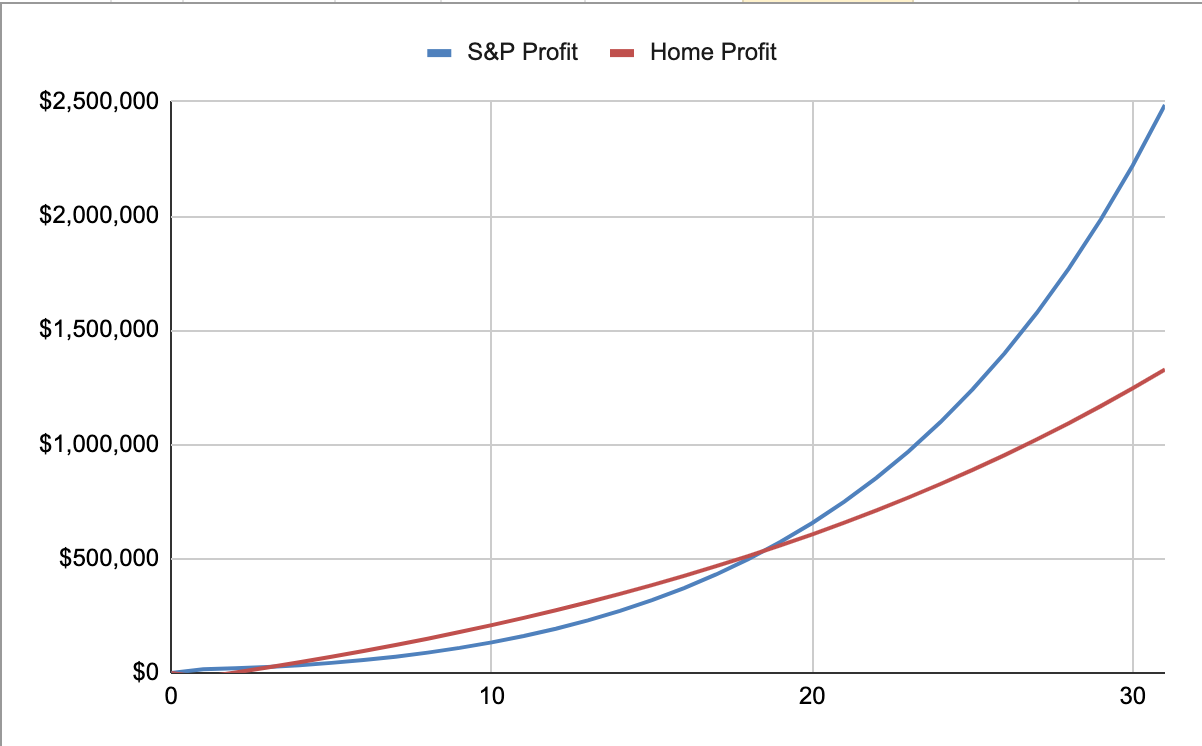

Next, let’s plot our investment profits over time (home value plus rental income minus interest, tax, and maintenance costs). We get Figure 5 below. Again, this is the “buy the boat” option, that doesn’t invest the down payment money of $84,000.

Zoom image will be displayed

We see that both options are good investments, each with their own pros and cons. The house investment gets us a nice place to live, hopefully in a nice neighborhood, and in addition is a solid investment. The stock market gives stronger returns, but can also be hair-raising when the market fluctuates.

The Final Tally

My Father’s advice was always to buy the biggest house one could possibly afford. Good advice? You decide. We’ve seen that buying a house and investing in the stock market are both good investments, each with its own headaches, risks and rewards. Going all in on the stock market gets you the biggest portfolio. The best advice, I think, is to do what’s right for you.

As for me, I do love my modest little house.

I built Gizmo Life Planner for my own use and entertainment, but you’re free to use it too. If you find any bugs or would like to see some enhancements for your particular circumstance, please reach out to me through the comments.