What's the Best Age to Start Collecting Social Security?

Learn how to maximize your Social Security benefit

You're 62 and maybe now is the time to retire. After all these years of funding the retirement of others, you can finally start collecting Social Security. Should you start now or wait?

There are a lot of factors at play here, way beyond when to start collecting Social Security, which makes a comprehensive analysis tricky. Let's investigate just this question — the title of this Story.

The Very Best Decision

Let's get the obvious out of the way. The best possible financial decision is to postpone retirement until you are 70. If your goal is to bequeath the maximum amount to your kids, then wait. Case closed.

On the other hand, have a look at the Actuarial Tables published by the Social Security Administration (SSA). If you're 62 and you're male, you've likely got 19 years left on planet earth (female, 22 years). Eight years (retirement at 70 — retirement at 62) is 42% of your remaining party time. Yikes. Suddenly, retirement at 62 looks pretty good, finances be damned.

It's Not Rocket Science

Let's say we've decided the time is right, we're retiring at age 62. We've got to decide when to start collecting.

The maximum Social Security Benefit, today, looks like this by retirement age:

- At age 62: $2,710/month

- At age 67: $3,822/month

- At age 70: $4,873/month

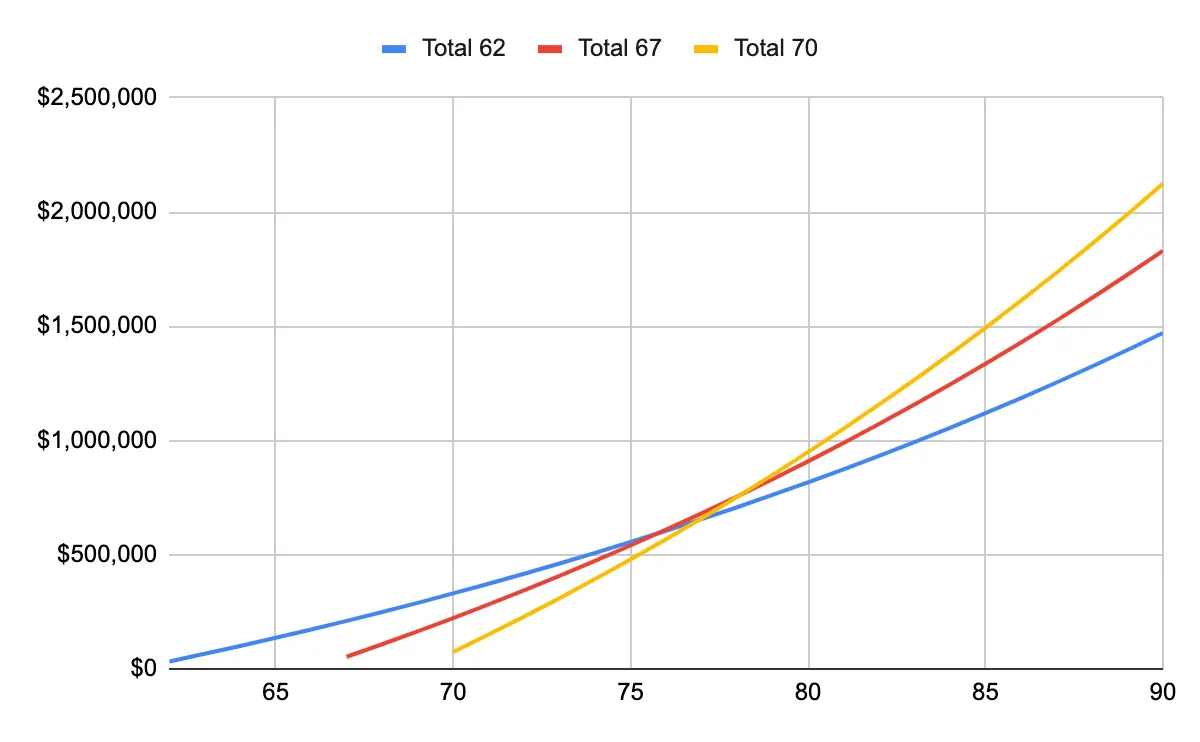

Let's assume a slightly optimistic yearly COLA (Social Security's cost-of-living increase) of 3%, and have a look at the lifetime total distribution from Social Security starting at those three ages.

Comparing total benefits for Social Security by Withdrawal Age (62, 67, 70)

That makes it easy right? The crossover is at age 77 (not coincidentally, about the average lifespan in the U.S. from birth). If you die before age 77, you'll be better off the earlier you start collecting.

On the other hand, if you live to age 90, you'll make about $650,000 more if you waited until age 70.

Place your bets.

Not So Fast

We forgot something. Since we've retired at 62, we've got no income. If we decide to start collecting at age 70, we still need to live on something, and that something comes from our investments. The stock market earns an average of 10% and the bond market earns an average of 3–4%. Let's suppose we've balanced our portfolio to earn a relatively safe 5%. We've got to pull money from those investments to fund our blue plate specials.

The total income from Social Security from age 62 to age 70 (assuming we started collecting at 62) is $172,000. If we retire at 70, with no supplemental income, we are effectively "withdrawing" that $172K from our investment accounts, earning away at 5%.

That $172K will grow to a whopping $670K at age 90, a profit of nearly $500K. At age 82 (your life expectancy if you are 62) your profit is $240K.

Based on the age we start collecting, our total earnings at age 82 (life expectancy) from Social Security are:

- Start Collecting at 62: $930K

- Start Collecting at 70: $1,156K

And the difference is: $224K.

So we see that the difference between collecting at 62 and keeping additional money invested at 5% nets out to about the same as drawing on our investments and postponing Social Security until 70.

In other words, it doesn't matter much. Pick your poison.

What Will I Do?

I'm still working and I haven't decided. I'll cross that bridge soon enough. Though, my current thinking is that it's best to start collecting as soon as you can, and try to preserve your investments for as long as possible. Given a National Debt of $35 Trillion, it seems pretty clear that something's going to give, likely in my lifetime. I think Social Security isn't the guaranteed income it once was, so best to get it while you can.

On the other hand, there's no telling what the markets will do when that bill comes due, and those investments could tank.

Predicting the future is tough, so again, pick your poison.